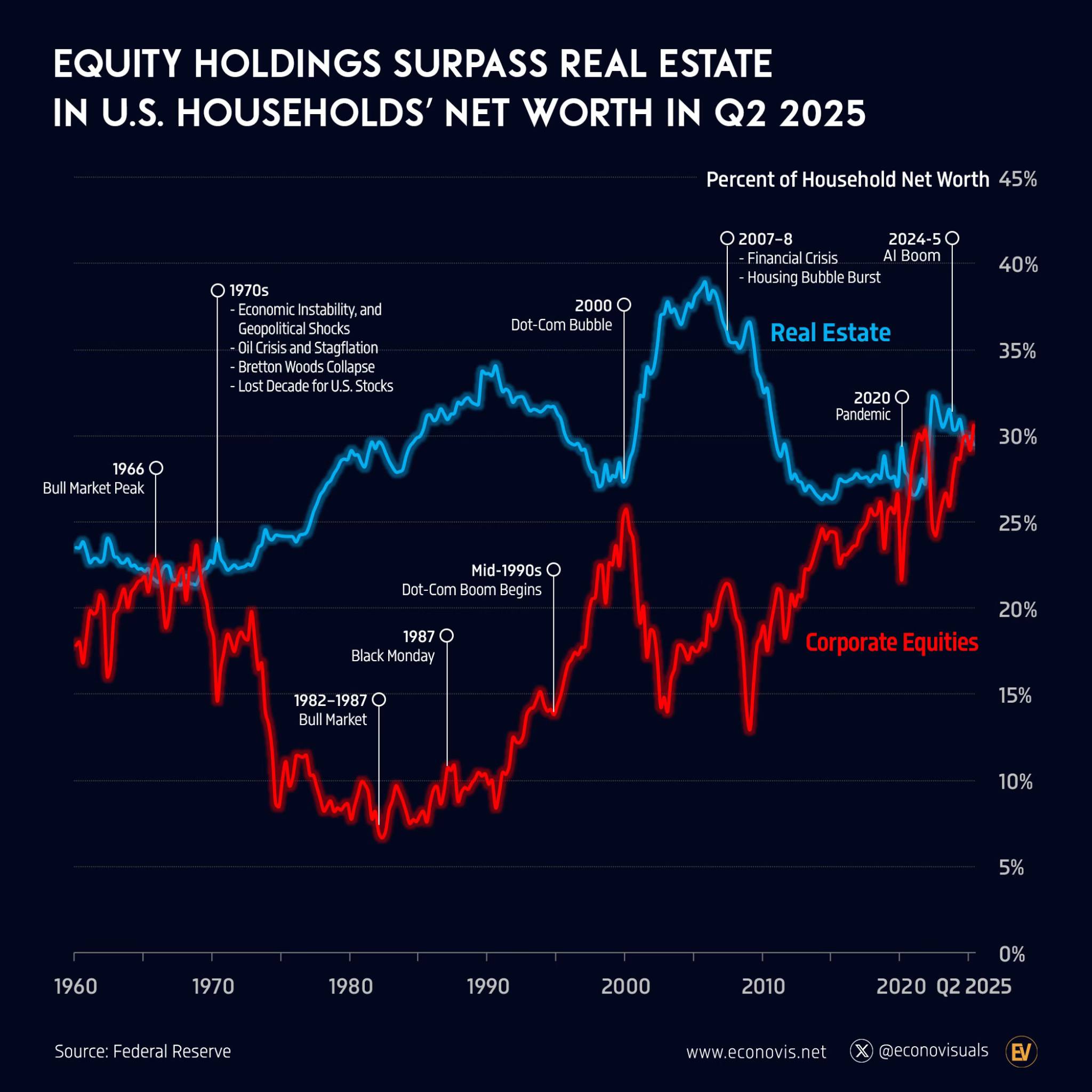

American households are experiencing their third major asset allocation reversal in 65 years. Data from the second quarter of 2025 shows that stocks and mutual funds account for 31% of household net worth, reaching a record high, while real estate has fallen below 30%. This is not a simple shift in investment preference, but a gamble for high growth in exchange for balance sheet stability. The personal savings rate in the U.S. is at a historical low, and when 31% of wealth is tied up in stocks that fluctuate every second, a liquidity slaughter is counting down.

U.S. Household Wealth Anchor Breaks: U.S. Stocks Overwhelm Real Estate

(Source: Econovis)

For the past half century, the wealth anchor of the American middle class has been real estate. Houses not only provide living functions but are also the core tool for wealth accumulation across generations. However, this anchor will be completely severed in 2025. Data shows that the proportion of U.S. stocks in household net worth surged from 25% in 2020 to 31% in 2025, while real estate plummeted from 38% in 2006 to below 30%. This marks the third time in 65 years that the proportion of stock assets has exceeded that of real estate.

The first two correspond to the frenzy of the 1960s and the internet bubble of 2000, both accompanied by severe adjustments after each reversal. The “Nifty Fifty” myth of the 1960s collapsed during the stagflation of the 1970s, and the tech bubble of 2000 led to a 78% fall in the Nasdaq. Historical patterns show that when the stock proportion breaks through the 30% threshold, systemic risks rise sharply.

The driving force behind this reversal comes from multiple aspects. First, the Federal Reserve's ultra-low interest rate policy has been maintained for nearly 15 years, driving the stock market to continue rising. Second, the popularity of 401(k) retirement plans and index funds has transformed stock investment from an elite game into a nationwide activity. Third, the real estate market suffered a confidence hit after the 2008 financial crisis, leading the younger generation to question the logic of “getting rich by buying a house.” Fourth, the wealth creation myth of tech giants, with companies like Tesla, Nvidia, and Apple generating wealth effects far exceeding that of real estate.

However, changes in the asset structure have brought about a qualitative change. Although real estate rises slowly, it does not quote daily, providing a sense of psychological safety. In contrast, US stocks fluctuate every second, and when 31% of the wealth in society becomes K-line charts, the overall volatility of wealth is artificially magnified several times. This means that the Federal Reserve cannot allow a bear market to occur – a 20% drop in US stocks would severely impact consumer confidence, far exceeding the real estate crisis of that year.

The Essential Difference Between AI Revenue Realization and That of the Year 2000

Seeing that “the proportion of US stocks has reached a new high,” many investors who experienced the internet bubble in 2000 may instinctively feel fear. At that time, the proportion also peaked at 25%, followed by a crash. However, simply “looking for a sword in the boat” is wrong, as the underlying logic supporting the market has undergone a qualitative change.

The tech stock bubble of 2000 was built on the hype of the concepts of “click-through rates” and “eyeball economy,” with leading tech companies having meager revenues or even losses. Star companies like Pets.com and Webvan had traffic but no cash flow, with market-to-sales ratios reaching hundreds of times. In contrast, the AI giants of 2025 possess terrifying earning capabilities. According to forecasts, OpenAI alone is projected to surpass $20 billion in annualized revenue by the end of the year, with a gross margin as high as 70%.

This difference is crucial. Tech giants like Microsoft, Google, Meta, and Amazon not only have enormous market values but also possess robust cash flow and profitability. Although their valuations are not low, they are far from the madness of 2000, which was completely detached from fundamentals. This bull market is built on “real cash” cash flow, rather than merely on market dreams.

However, this does not mean that there are no risks. The monetization cycle of AI investments still carries uncertainty, and whether the capital expenditures of ultra-large data centers can translate into sustained revenue growth needs time to verify. The more critical issue is that even if the fundamentals of tech giants are sound, when American households have 31% of their wealth bet on the stock market, any external shock could trigger a chain reaction.

Liquidity trap asset wealth and cash scarcity fatal scissors difference

The real risk is not in the numbers of stock accounts, but in the depletion of bank deposits. American households are facing a deadly liquidity mismatch: the asset side has never been so rich, with stock account values reaching new highs; yet the cash side has never been so tight, with personal savings rates at historical lows and credit card default rates on the rise.

This phenomenon of “wealthy poor” has formed a significant risk scissors gap. In today's environment of “everyone holding stocks” and “low savings”, American households are essentially “running naked”. They assume that stocks can be liquidated at any time to pay bills, but once the US stock market experiences a normal 10% pullback, many households will be forced to sell stocks to sustain their living due to the lack of a cash buffer.

Four Triggers of Liquidity Massacre

1. External shocks trigger a stock market correction

· Rising Japanese bond yields lead to a tightening of global Liquidity.

· Geopolitical crisis impacts risk assets

· The Federal Reserve's policy shift exceeded expectations

· The AI bubble burst triggers a collapse in tech stocks

2. Forced liquidation mechanism activated

· Cash-strapped families sell stocks to pay bills

· The surge in credit card default rates triggers banks to tighten credit.

· Margin call forced liquidation leveraged positions

· Mutual funds face redemption pressures leading to accelerated sell-offs.

3. Liquidity Crisis Self-Reinforcement

· Selling pressure drives stock prices to further fall

· The reversal of the wealth effect hits consumer confidence.

· The downward revision of corporate profit expectations intensifies panic

· Market liquidity dries up and price discovery fails.

4. The Dilemma of the Federal Reserve's Market Rescue

· Interest rate cuts to rescue the market may exacerbate inflationary pressures.

· The asset purchase plan faces ethical risk concerns.

· It may be difficult to seize the market rescue timing, potentially missing the best window.

· The market's over-reliance on the central bank creates a fragile balance.

This “forced selling” mechanism amplifies what would have been a normal market adjustment into a liquidity crisis in an instant. Historically, the Great Depression of 1929, Black Monday in 1987, and the financial tsunami of 2008 all exhibited similar characteristics of liquidity exhaustion. When everyone rushes for the exit at the same time, the width of the door determines the severity of the stampede.

Recognizing reality and seeking survival amidst fluctuations

Whether you like it or not, your wealth fate is already tied to the US stock market. At this moment, holding a large amount of cash may underperform against inflation, but having no cash at all is suicidal. The key is balance: as long as the revenue growth of tech giants (like OpenAI's $20 billion threshold) can continue to materialize, the bubble will not easily burst. But the biggest risk is not the fall in stock prices, but that you have no money to spend when stock prices fall.

It is recommended that investors ensure they have at least 6 months' worth of living expenses on hand and not invest their last penny in the U.S. stock market. Although real estate may not yield returns as high as stocks, the stability and Liquidity it provides is crucial during times of crisis. In an era of 'growth through volatility', surviving is winning. When 31% of wealth is on the roller coaster, fastening your seatbelt is more important than chasing speed.