Original Title: Has the Global Recession Begun?

Original Author: Capital Flows

Translation: Peggy, BlockBeats

Editor’s Note: While markets continue to debate “whether a recession has begun,” this article shifts the perspective forward to focus on the constraint structure behind it. At present, the linkages among energy shocks, geopolitical dynamics, and monetary policy are reshaping a more complex macro environment. In this environment, central banks no longer have a clear reaction function; the traditional path of rate hikes or cuts fails at the same time, and policy space is effectively “locked.”

The article redefines recession not as an “economic outcome,” but as a “strategic condition.” It not only compresses growth and employment, but also weakens a country’s bargaining power, ability to attract capital, and external credibility—thereby causing it to lose initiative in global competition. For exactly this reason, governments around the world are replacing monetary tools with fiscal, diplomatic, and even geopolitical measures. In essence, they are buying time for growth to slump, while avoiding being forced into negotiations during a recession.

Within this framework, the market’s core is no longer the interest-rate path itself, but “who can escape the constraints, and who remains trapped.” This difference first shows up in foreign exchange and interest-rate markets, and then propagates into asset prices and capital flows. When valuations keep rising even as growth slows, the reason may not be an improvement in fundamentals, but rather policy expectations of “a recession that will not be allowed to happen.”

When energy, capital, and power become re-intertwined, macro issues are no longer just economic issues, but a systemic game that spans policy boundaries.

The following is the original text:

This report is not trying to make predictions; it is attempting to reconstruct a possible structure: if the current energy shock continues to spill over and evolves into a global recession, what structure will this process take?

This kind of recession will very likely not unfold along the familiar path, but instead transmit through the financial system in a way that lacks clear historical reference, layer by layer, gradually amplifying. It is worth emphasizing that “whether something happens” and “how it happens” are two completely different things—and what this article cares about is the latter.

It also needs to be said clearly that I don’t believe this scenario is necessarily destined to occur. Honestly, I’m not the kind of “smart money” that went long crude oil and short stocks over the past month and then kept riding it all the way through to realize profits. My biggest risk exposure right now is actually in the Hyperliquid ecosystem—it has quietly benefited from geopolitical volatility and is one of the few assets that still posted positive returns within a few years, while “the seven big U.S. tech stocks” and Bitcoin are, overall, in a drawdown range.

I’m bringing this up simply to explain: the most dangerous thing in the market is never getting the direction wrong; it’s taking a position first, and then building a framework to interpret the world around it.

The problem is that this system itself assumes everything

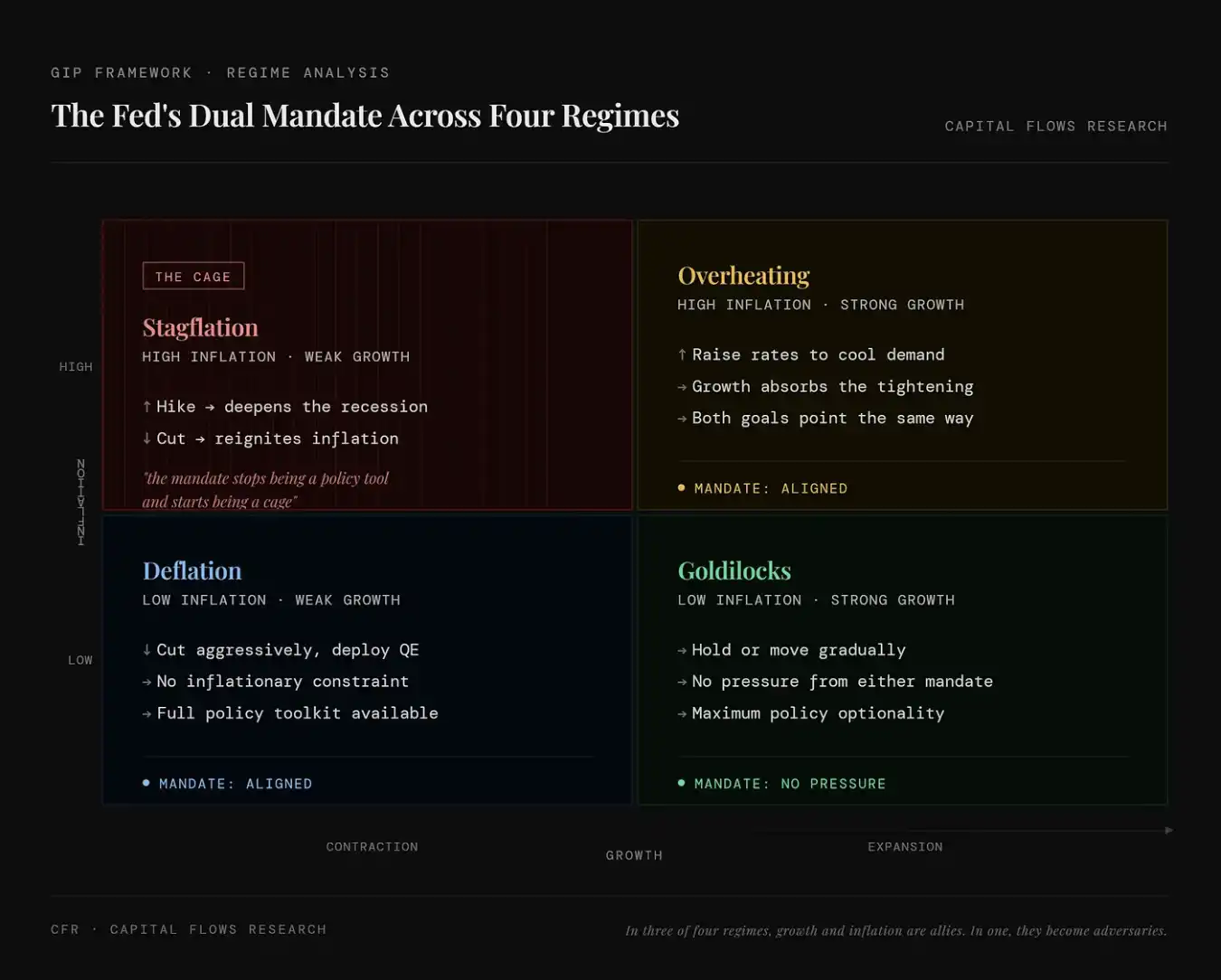

Supply shocks are one of the variables that are among the few capable of breaking conventional economic relationships. In most cases, growth and inflation move in the same direction: the hotter the economy, the higher prices go; the colder the economy, the inflation cools. Macroeconomic policy is designed around this relationship, and the underlying logic of the modern central banking system is built on this assumption as well.

The Federal Reserve’s wording is very typical: “Our dual mandate is to achieve maximum employment and price stability.”

Behind this definition, there is actually an implicit premise—that growth and inflation are largely compatible. In the vast majority of cases, this premise holds. But in one particular kind of scenario, they end up offsetting each other. Once you enter this state, the “dual mandate” is no longer a policy tool that can be operated; it becomes more like an invisible constraint.

This chart shows how the Fed’s dual mandate (“jobs + inflation”) performs across four economic states. Upper left (stagflation) indicates high inflation alongside low growth; in this environment, whether you hike or cut rates creates new problems, policy goals conflict with each other, and the dual mandate turns from a tool into a constraint; upper right (overheating economy) indicates high inflation alongside high growth; in this case, rate hikes can curb inflation without immediately harming the economy, so the directions of the two goals are aligned and policy is relatively easier to implement; lower left (deflation) indicates low inflation alongside low growth; in this environment, you can comfortably cut rates and loosen liquidity to stimulate the economy without being constrained by inflation, leaving ample policy space; lower right (Goldilocks) indicates low inflation alongside high growth, where both the economy and prices are at ideal levels—policy requires little intervention, and flexibility is highest.

This “constraint” is not a theoretical assumption. Since the late 1990s, the pricing environment with stagflation characteristics has appeared in less than 10% of market time. Among the economic states listed in the table below, it is the rarest one, yet it corresponds to the worst asset returns—especially for mainstream assets that most people hold.

This chart quantifies the frequency of different macro states and their impact on asset prices. Each row corresponds to a market combination: stocks (up/down), rates (up/down), and the dollar (strong/weak), and provides three key metrics: FREQ (how often that state appears), AVG DUR (average duration), and SPX / 10Y / DXY (how stocks, Treasuries, and the dollar perform in that environment).

The scenario pointed to by the red arrows in the chart is “Stocks Down / Rates Up / Dollar Up”—meaning stocks fall, interest rates rise, and the dollar strengthens. The frequency of this state is about 9.8% (under 10%). Stock returns are negative; rising rates mean bond prices decline. At the same time, a stronger dollar corresponds to tighter overall conditions, typically a stagflation or tightening-type shock environment. While this environment is not common, it is often the most damaging: stocks fall (risk assets get hit), bonds fall (rates rise), and the dollar strengthens (liquidity tightens), which means common stock-bond combinations are under pressure at the same time. In other words, it is the rarest macro state (about 10%), and it also tends to correspond to the worst asset performance, because there is essentially no true “safe haven.”

This is exactly the moment we’re in right now. The reason volatility is so intense and people are so panicked is not because a recession is already inevitable; it’s because we are in the only scenario where, no matter what the Fed does, it will worsen another problem while solving one.

Transmission chain

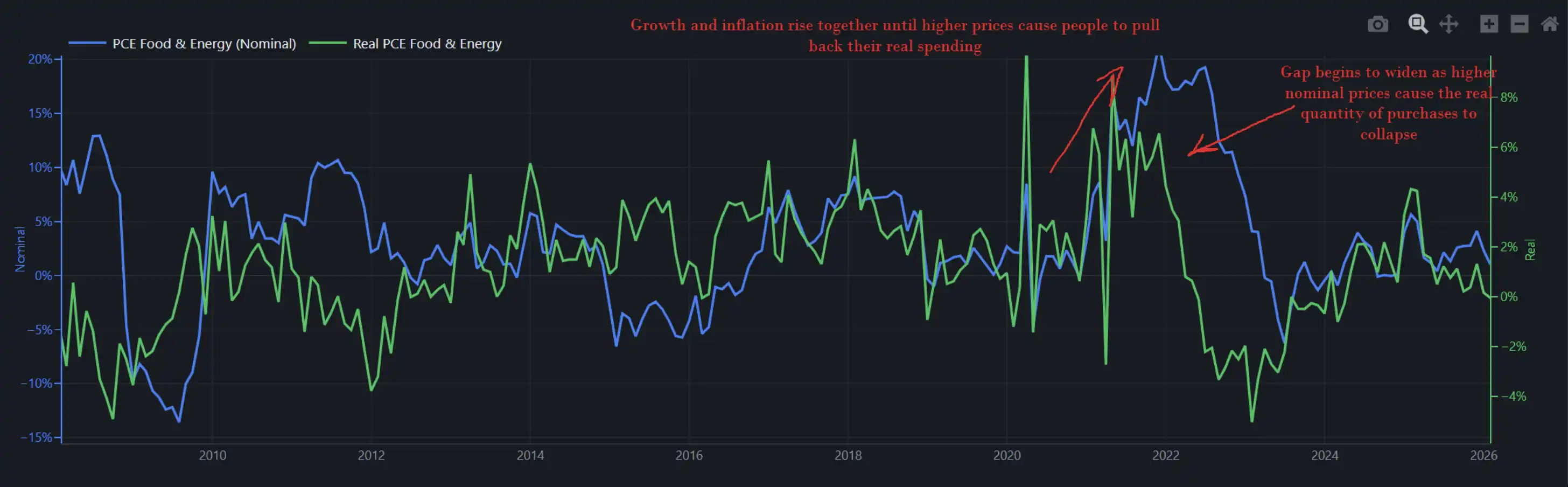

The chart below shows the nominal and real changes in food- and energy-related spending in the economy. In other words, it simultaneously reflects how much American consumers “actually spent” (quantity) and “were charged for” (price).

When growth and inflation rise together, higher prices do not immediately destroy demand. People choose to bear it—complaining while also pushing for wage increases—while continuing to consume. 2022 was exactly like this, which is also why the Fed was able to keep hiking rates in that kind of environment without immediately triggering an economic collapse. At that time, real consumption year-over-year growth was close to 8%, meaning the economy itself had the capacity to withstand the shock.

This chart shows the divergence process between nominal spending (blue line, price × quantity, representing how much was spent) and real spending (green line, quantity purchased, representing how much people actually bought): in the early stages of inflation, both move upward together, indicating that price increases have not yet suppressed demand and consumers are still “absorbing” the shock; but once prices keep rising, nominal spending continues to increase while real spending begins to decline—there is a clear divergence between the two, meaning that high inflation has started to erode real purchasing power and squeeze demand. In other words, inflation does not immediately destroy consumption, but once it crosses a certain threshold, it shifts from something “bearable” to something “cut back,” becoming a key variable that drags on the economy.

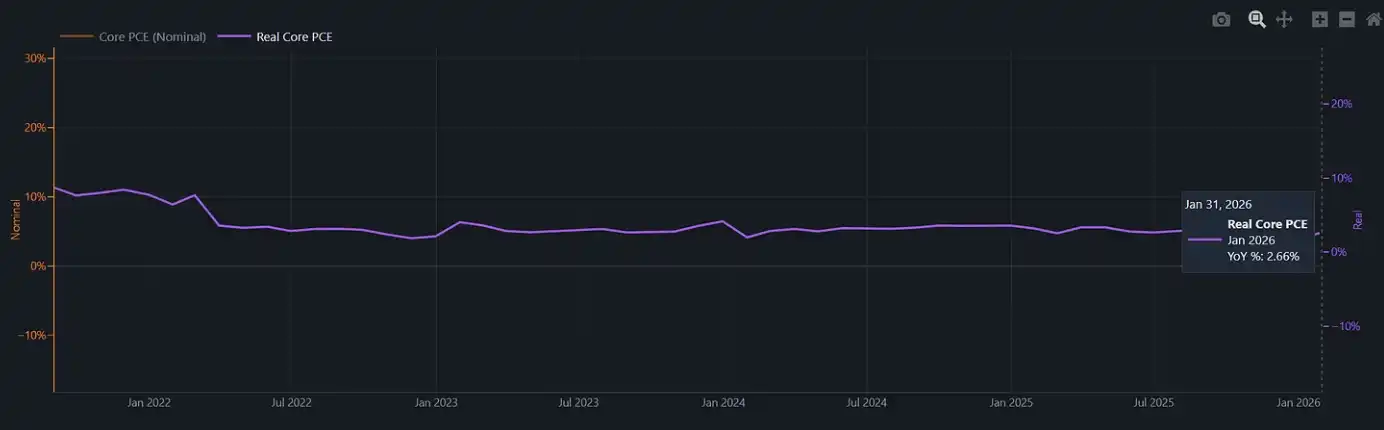

Our current real spending year-over-year growth rate is roughly around 2% (whereas in the previous energy-shock cycle in 2022, this figure was close to 8%).

This chart shows Real Core PCE—core real consumption, excluding inflation

In 2022, the Fed was raising rates in an economic environment that still had enough momentum to withstand tighter financial conditions. But that buffer no longer exists. If another round of an inflation shock emerges now—for example, food CPI historically typically lags energy shocks by three to six months and then rises—the Fed would face a policy environment with almost no “exit pathway that looks dignified.” With real consumption at only about 2%, continuing to hike rates could directly crush consumers; but choosing to stand pat and allow inflation to rise again would be tantamount to confirming that it is trapped in a “cage.”

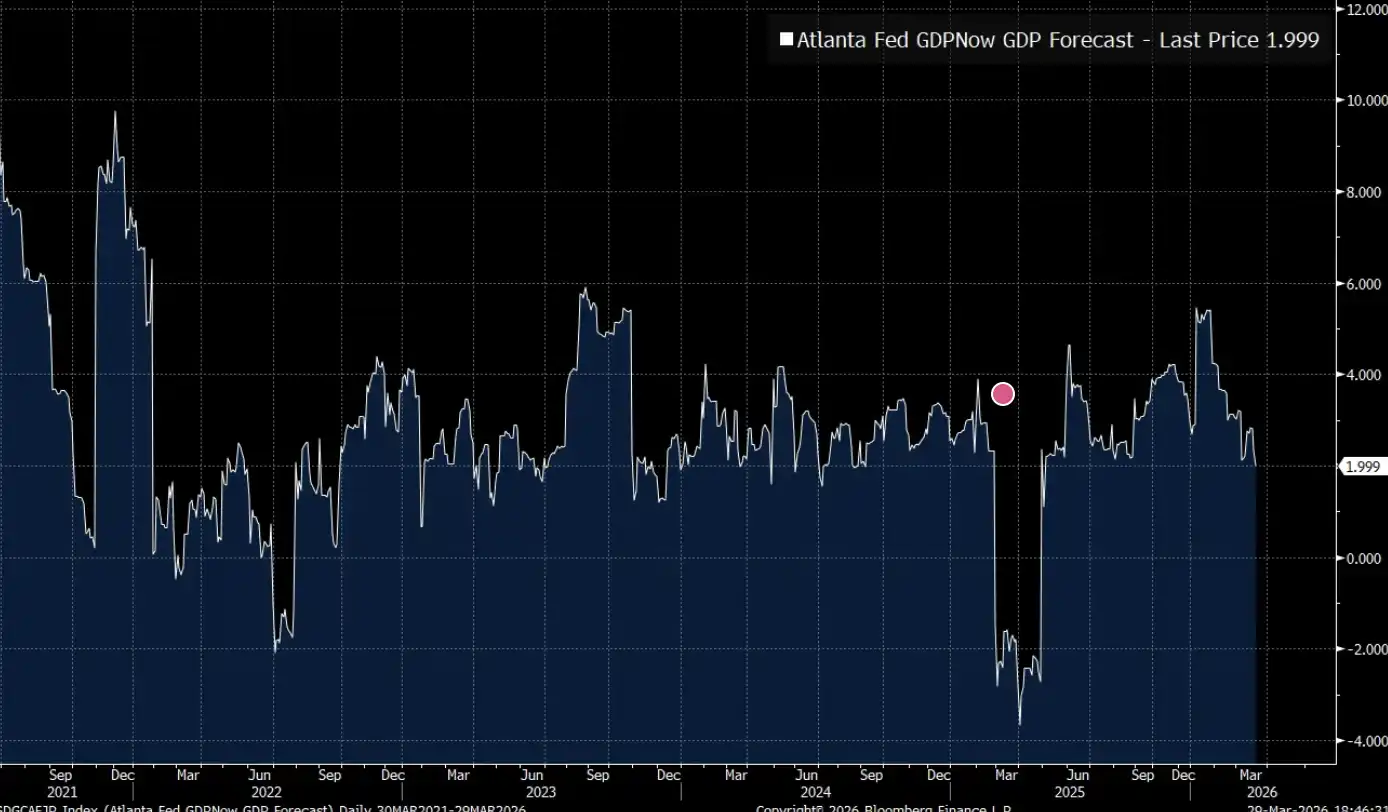

The GDPNow forecast from the Federal Reserve Bank of Atlanta has just fallen below 2%.

The Atlanta Fed’s GDPNow (real-time GDP forecast) shows that the U.S. economy is currently running in the roughly 2% “critical growth” range: it has not fallen into recession, but there is very limited room to absorb additional shocks.

Geopolitics

There is one analytical path that stops at the commodity prices themselves: oil prices rise, input costs rise, central banks are constrained, and growth slows. For many investment portfolios, this framework is already complete enough. But at minimum, we need to admit that energy shocks do not occur in a vacuum.

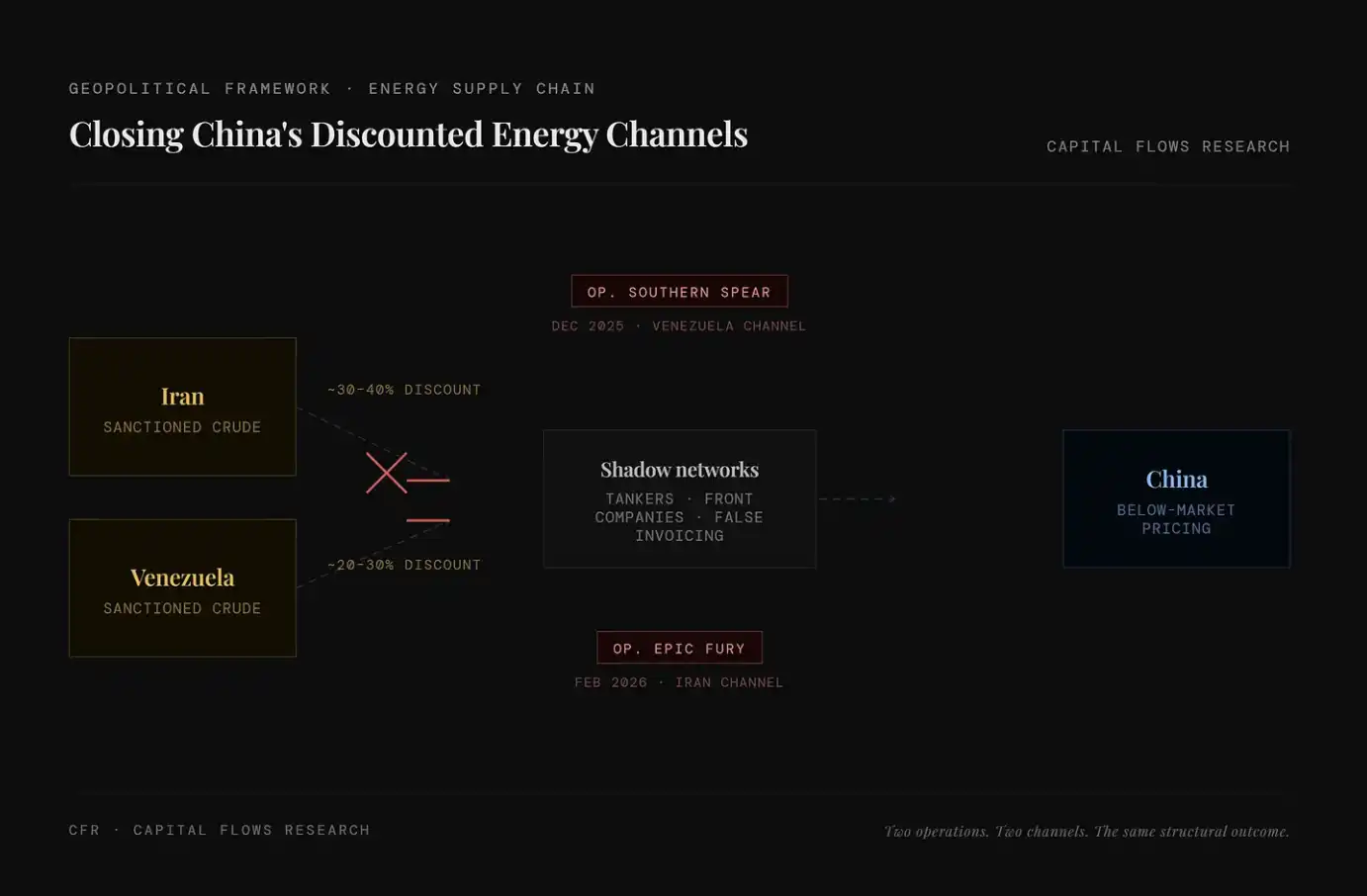

Over the past two years, the U.S. has been systematically tightening the channels for China to obtain low-priced energy, including Iranian crude oil and Venezuelan crude oil—resources that had been flowing through “shadow networks” at far below market prices. As for whether “Operation Epic Fury” had such strategic considerations, or whether it merely accelerated an already unfolding trend, that question is outside my ability to judge. What I can observe is the overall structure revealed by this process.

On the left side of the chart are two discounted energy sources: Iranian crude oil (about a 30–40% discount) and Venezuelan crude oil (about a 20–30% discount); in the middle is the “shadow network,” composed of tankers, shell companies, fake invoices, and so on, used to bypass sanctions and deliver these low-priced crude oils to the market. The key change is that this system is being systematically cut off: the “Op. Southern Spear” in 2025 targets the Venezuelan corridor, while the “Op. Epic Fury” in 2026 targets the Iranian corridor—meaning that two major discounted energy pathways are being closed. As a result, low-priced supply is gradually removed, and the bottom of global energy costs is lifted.

Reporting focused on Jared Kushner tends to concentrate on an “ethical narrative” layer: on the one hand, he serves as Trump’s chief Middle East negotiation representative; on the other, he raises $5 billion from Middle East sovereign wealth funds, and those funds come from the very government he is negotiating with.

But compared with the ethical issue, what I care more about is the operational logic reflected by this behavior. Kushner is not acting impulsively, and his team is not thrown together on the spur of the moment. When the “deal layer” is operating at such high frequency and intensity within a short time, it often means there is a clear set of structural arrangements behind it: this administration is treating military actions, economic leverage, and capital flows as linked tools within the same system.

In other words, this is not random action, but a sequence of actions being designed and carried forward.

Note: The private equity fund Affinity Partners founded by Kushner is mainly funded by Middle East sovereign wealth funds. His background in handling Middle East affairs during his time in the White House has kept his financing activities consistently sparking controversy about the boundaries between political relationships and capital flows.

For the purposes of this article’s discussion, the more critical point is this: this round of oil-price shocks is not an occasional “weather event.” It has drivers, and it has beneficiaries. This point will directly affect how you judge its duration and how policy should respond.

Recession: a strategic vulnerability

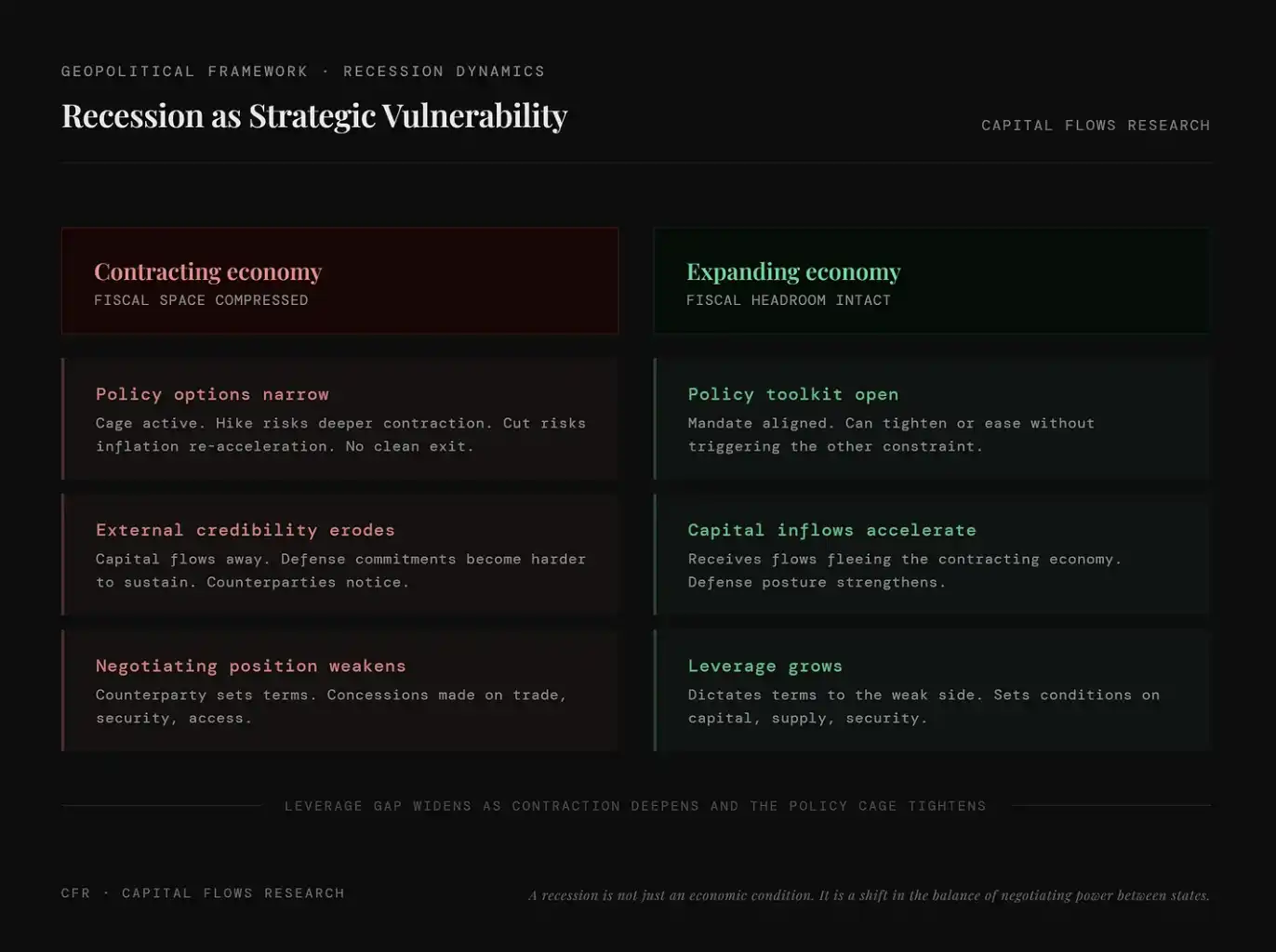

The traditional understanding of recession is economic: output contracts, unemployment rises, and central banks intervene. But the framework used here is different—it incorporates the incentive structure of geopolitics together with economic logic.

A recession is not only an economic condition; it is also a redistribution of bargaining power structures among countries.

The mechanism is not complicated: once a country falls into recession, its fiscal space, political capital, and external credibility all shrink at the same time. Governments cannot use resources that do not exist, and central banks also find it difficult to restore normal policy without worsening the contraction. And the counterparties in its negotiations—in trade, security, capital markets, and more—will all notice this and factor it into the negotiation terms.

By contrast, countries that can avoid recession, or only enter it “later,” sit on the other end of the scale. They can dominate the rules, attract capital flowing out of shrinking economies, and accumulate strategic leverage that would otherwise need to be consumed by the opposing side just to keep the system running.

This chart compares the positional differences of contractionary and expansionary economies in geopolitics: the former faces compressed fiscal space, limited policy choices, declining external credibility, and weakened negotiation capability; the latter has more ample policy tools, ongoing capital inflows, and constantly increasing bargaining power. In other words, recession is not only an economic issue—it also means that a country is disadvantaged in global games, while growth itself will be transformed into real strategic leverage.

This is nothing particularly new or insightful; it is the oldest logic in governance. The special aspect of the current moment is that this mechanism is operating in a particular environment: the central banks of the major importing economies are already constrained by the “cage” described earlier.

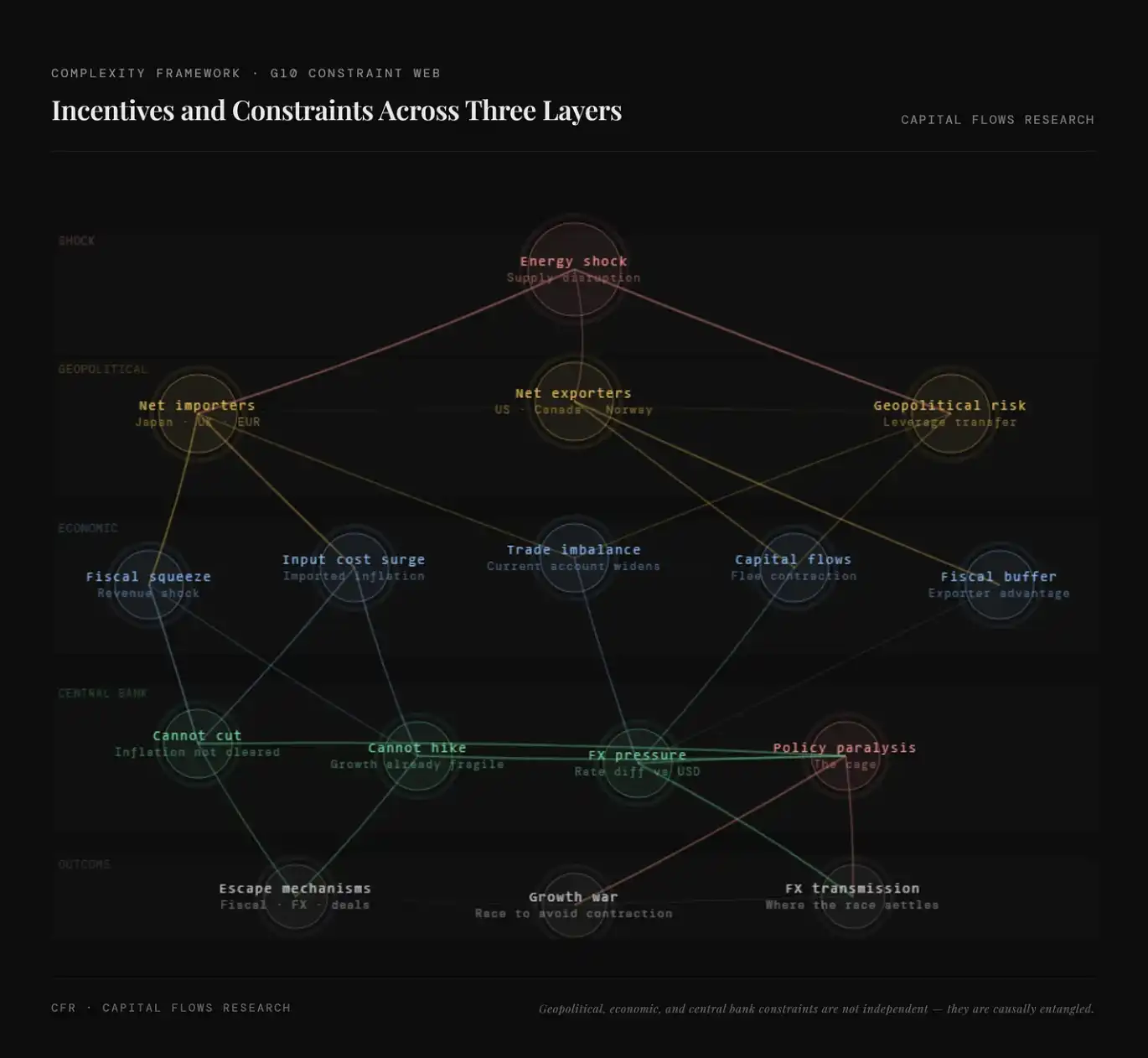

In such an environment, the G10 is not a homogenous whole; it is divided by the energy structure. The U.S., Canada, and Norway are net oil exporters. When oil prices rise, their energy sectors expand, and the inflation structure facing their central banks is entirely different from that of other countries. By contrast, Japan, the U.K., Germany, France, Italy, and most eurozone countries are net importers. Every time oil prices rise, it directly feeds into their production costs, trade balances, and overall inflation levels. In a world where oil is used as a geopolitical tool, they are essentially on the side “shorting energy.”

This “cage” also lands differently across these two types of countries. For net exporters, even under global stagflation pressure, they can still rely on energy revenues and related jobs to create a buffer. For net importers, however, they bear the inflation shock without income offsets. Their central banks cannot ease (because inflation has not faded), and they also cannot tighten further (because growth is already fragile). Structurally, these constraints put far more pressure on energy net importers than on Washington.

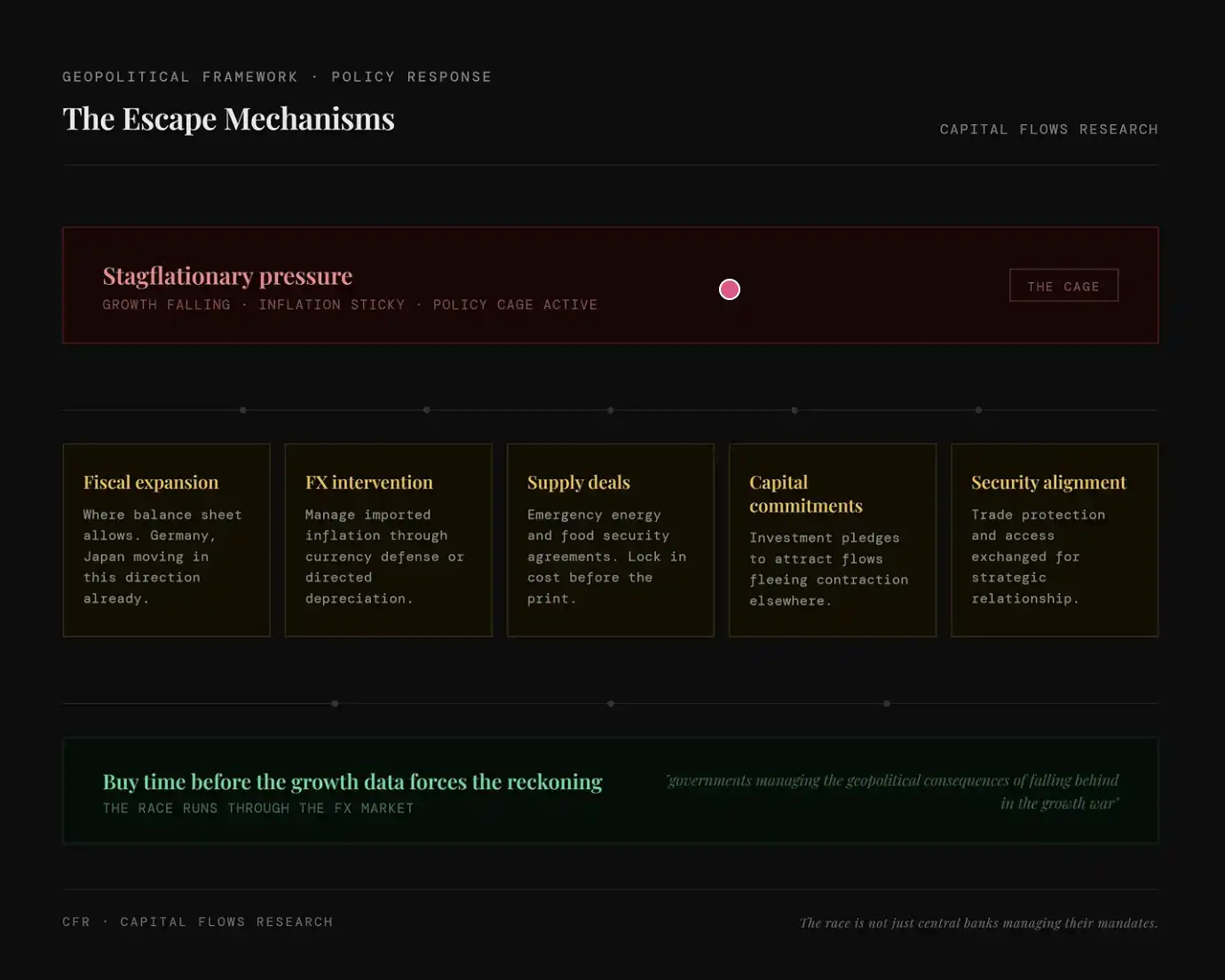

In a “stagflation + policy constraints” environment, countries are not without options—they are looking for alternative paths to “work around the central bank.” For example, fiscal expansion, using the government’s balance sheet to backstop (e.g., Germany, Japan); foreign exchange intervention, using currency hedging to offset imported inflation; supply lock-in, signing energy/food agreements in advance to lock in costs; capital commitments, attracting capital inflows through investment to offset economic contraction; security alignment, using security/political relationships in exchange for trade and resources.

Geopolitics, economic conditions, central bank constraints, and the incentive mechanisms running through them

At the geopolitical level, the key is not competition among the individual importing economies, but their relationships with the forces that benefit from their weakening. A country stuck in recession becomes a more “easy to talk to” trade partner, a less reliable security guarantor, and is also more likely to become a target of patient, long-term penetration. And China especially has shown a willingness to pursue this strategy. China does not need to actively “attack” a weakening economy; it just needs to wait, provide financing, lock in supply relationships, and gradually gain structural dependence during the counterpart’s negotiation process as it transitions from strength to weakness. Recession is precisely the condition that makes all of this possible. Therefore, avoiding recession is not only an economic objective—it is a strategic objective. Governments in all the energy net importing blocs essentially understand this, even if they may not state it in those words.

At the economic level, the core incentive is: “buy as much time as possible” before growth worsens further and forces policy into more disorderly reactions. Through supply agreements, lock in costs before the next round of inflation data is released; through investment commitments, attract capital that might otherwise flow out due to recession expectations; through trade arrangements, replace the price mechanism that has already failed. These measures are not exactly “clean” solutions, but they are still better than another scenario—being forced to go to the negotiating table during a recession.

At the level of central banks, the constraints are the most explicit and also the hardest to resolve. In the absence of inflation having fallen yet, cutting rates prematurely could further entrench inflation. But standing pat when growth keeps weakening could trigger a demand collapse, making the cost of the next round of easing higher. For energy net importing countries, the situation is even more complicated: their inflation path depends, to a certain extent, on the Fed’s decisions rather than being fully driven by domestic policy. As interest-rate differentials change, the domestic currency moves relative to the dollar, and imported inflation adjusts accordingly. So how tight or loose this “policy cage” is depends partly on choices made in Washington—not on Frankfurt, Tokyo, or London.

This chart systematizes the multi-layer transmission chain triggered by an energy shock: starting from supply disruptions, propagating along geopolitical divisions (net importers vs. exporters, leverage transfers), then through economic variables (rising costs, fiscal squeeze, trade imbalances, and capital flows), and ultimately evolving into policy constraints at the central bank level (not able to cut rates and also difficult to raise them). It finally turns into policy paralysis and a “growth race.” The core meaning is that the current shock is not a single inflation problem, but a systematic repricing process intertwined with energy, capital, and power structures.

Putting all the above strands together, we can see a clear environment: traditional central bank reaction functions have already failed, and governments are replacing monetary policy with fiscal and diplomatic tools. As a result, the resulting capital flows are no longer driven only by interest-rate differentials; they also depend on which economies manage to escape the constraints and which remain trapped. This distinction—“who is inside the cage and who has found an exit”—first shows up in the foreign exchange market. Fundamentally, the FX market is pricing a gap: the distance between where policy “should be going” and where it is “actually allowed to go.” When this gap expands at the same time across multiple major importing economies, cross-border capital allocation is no longer a secondary issue; it becomes the core issue.

Putting all the clues together

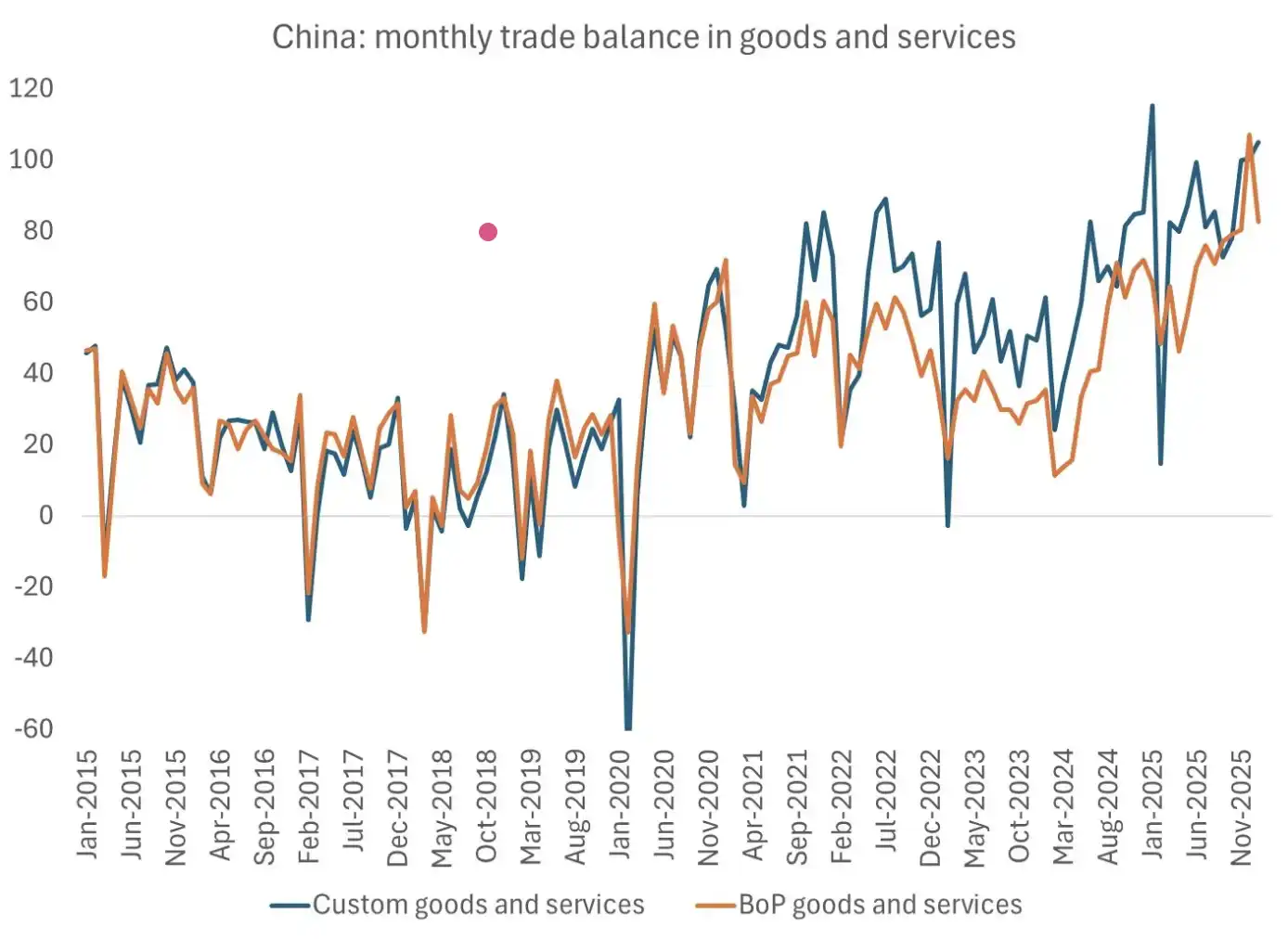

The truly worth thinking question is not whether a recession will occur, but whether the governments and central banks of the major importing economies will “allow” a recession to happen. When the last demand shock of a similar scale opened a window, China seized the opportunity. The recession in 2020 was a key turning point for China to establish its dominant position in global commodity exports. This position was not achieved through coercion, but because while other countries were busy responding to the crisis, China executed a clear strategic plan.

This chart shows China’s trade surplus has continued to expand over the past few years and has recently reached a high level. This indicates that during the recent shock cycle, China was not weakened—instead, by continuously expanding its trade surplus, it strengthened and consolidated its global export dominance. Chart source: Brad Setser

For the central banks in those countries currently trapped in the “policy cage,” they are well aware of this history. Therefore, the more worth focusing question is not whether they will continue to hike rates in response to the supply shock—thereby risking triggering a recession—but whether they will, without saying so explicitly, relax liquidity conditions, tolerate rising prices of financial assets, and allow valuation expansion in order to avoid bearing the political and strategic costs brought about by economic contraction.

This equity valuation chart can be seen as one way to interpret that choice. In a sense, the market may already be pricing in the answer.

Note: This chart compares the price-to-sales ratio (P/S) changes of the major stock markets in the U.S., Europe, Japan, and the U.K. It shows that against a backdrop of weakening growth, the valuation level of global equity markets has risen overall, and some markets are approaching or have already broken above their historical ranges. Its meaning is that current stock price gains are driven more by liquidity and policy expectations than by earnings improvement, reflecting the market pricing a policy stance of “avoiding recession and tolerating rising asset prices.”

I think once the market forms a consensus, macro commentators in the media who realize they have “only seen the trees, not the forest,” the market will experience a sharp repricing: first hitting the FX and interest-rate markets, and then spreading into an aggressive rush toward gold and silver. At that time, the central banks’ “inaction” will carry more weight than any statements they make at press conferences.

In my view, we are entering the final stage of the “endgame” in macroeconomics and geopolitics.

Tomorrow, Part Two. Foreign exchange and interest rates are precisely the core tools for pricing the above constraints and incentives. The implied premia and discounts embedded in these markets are the most direct signals we use to judge which economies global capital believes are “escaping the cage,” and which are still trapped. Next, we will build from here.

[Original Article Link]

Click to learn about Lydong BlockBeats recruiting positions

Welcome to join the official Lydong BlockBeats community:

Telegram Subscription Group: https://t.me/theblockbeats

Telegram Discussion Group: https://t.me/BlockBeats_App

Twitter Official Account: https://twitter.com/BlockBeatsAsia