TL;DR

- U.S. Manufacturing PMI (52.4, 2-month high) reinforced the “higher-for-longer” rate narrative, contributing to a 3.2% weekly decline in the S&P 500.

- 10Y Treasury yields (4.44%, mid-2025 high) reflect market pricing of persistent inflation driven by energy shocks and resilient growth.

- Geopolitical risk premiums remain elevated following Trump’s 48-hour ultimatum on the Strait of Hormuz (Mar 23), supporting safe-haven demand for USD.

- Crypto markets stayed weak last week. BTC fell 2.7% and ETH dropped 3.4%, while both BTC and ETH spot ETFs saw net outflows.

- TAO stood out with a 20.8% gain, driven by SN3’s successful training of a decentralized 72B-parameter LLM and additional attention from Jensen Huang’s positive remarks on Bittensor.

- BNP Paribas expanded crypto access via ETNs for French retail, signaling continued institutional distribution growth in Europe.

- Tether advanced toward its first full USDT audit, highlighting a strategic push toward transparency and U.S. regulatory alignment.

- NYSE-parent ICE invests $600M in Polymarket as exchange operators move deeper into prediction markets.

Macro Overview

U.S. Manufacturing PMI Hits 2-Month High, US Initial Jobless Claims Suggest Economic Downside Risks

The S&P Global US Manufacturing PMI climbed to 52.4 in March 2026, exceeding expectations of 51.3. This 2-month high indicates that despite high interest rates, the manufacturing sector is expanding. However, the S&P 500 fell 3.2% this week, closing at 6,368.85, as investors weighed strong economic data against the “higher for longer” interest rate narrative. The resilience in manufacturing output suggests that the economy is not yet cooling enough for the Fed to consider immediate rate cuts. Market volatility remains high as technical levels are breached, and the divergence between economic strength and equity performance widens.

U.S. initial jobless claims rose by 5,000 to a seasonally adjusted 210,000 for the week ended March 21, precisely aligning with market forecasts. While continuing claims fell to 1.819 million, the decline potentially reflects exhausted eligibility rather than robust hiring. From a macro perspective, the labor market exhibits a “low-hire, low-fire” equilibrium. Despite low layoff levels, businesses remain hesitant due to lingering uncertainty from aggressive import tariffs and Middle East volatility. This stability grants the Federal Reserve room to maintain interest rates at 3.5–3.75% while monitoring inflation risks. However, with the unemployment rate drifting toward 4.4%, the zero-employment growth environment suggests emerging downside risks for the broader economy.

The March 23 deadline regarding the Strait of Hormuz has intensified global energy risks. This critical chokepoint handles 20%-30% of global oil, and its potential closure keeps prices volatile. Simultaneously, the expansion of U.S. tariff investigations into markets like Vietnam and Taiwan creates a complex polycrisis for central banks. These supply-side shocks and trade barriers generate significant inflationary pressures. Consequently, the Federal Reserve faces a difficult task because these geopolitical factors remain beyond the reach of traditional monetary policy and domestic economic data.

The upcoming week focuses on the U.S. March non-farm payrolls report, with markets anticipating 180,000 new jobs and a 4.4% unemployment rate. Investors are also monitoring Eurozone inflation data and the ISM Manufacturing PMI for signs of economic resilience. These indicators, coupled with ongoing Middle East tensions and new tariff investigations against Vietnam and Taiwan, will likely dictate whether the Federal Reserve maintains its current interest rate trajectory amid a complex global polycrisis. (1)

DXY

DXY

DXY rose to 100.193 as geopolitical instability intensified following the March 23 deadline for the Strait of Hormuz. Investors sought the dollar as a safe-haven asset amid potential energy supply shocks and expanded tariff investigations. This risk-off sentiment, coupled with expectations of a cautious Federal Reserve, bolstered the greenback’s strength against major currencies. (2)

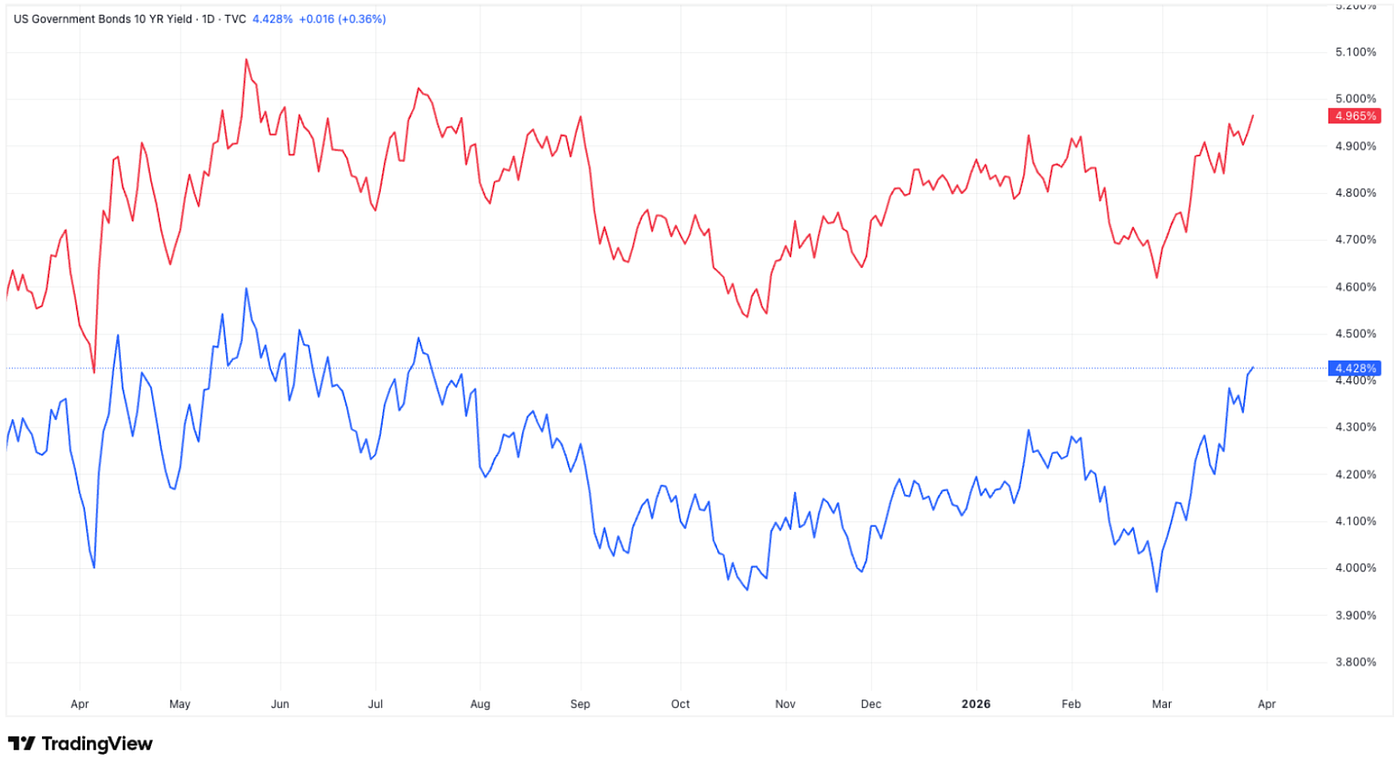

US 10-Year and 30-Year Bond Yields

US 10-Year and 30-Year Bond Yields

Treasury yields fluctuated before surging, with US10Y rising from 4.350% to 4.428% and US30Y from 4.921% to 4.965%, the highest since July 2025. This sell-off reflects a polycrisis environment in which escalating Middle East tensions and new trade tariffs against Vietnam and Taiwan are fueling inflation expectations, forcing investors to demand higher term premiums. (3)

Gold

Gold

Gold prices rose from 4,468.93 to 4,493.118 as a risk-off mood gripped global markets. This safe-haven demand intensified after the March 23 deadline for the Strait of Hormuz expired. Despite a slight extension for talks, persistent geopolitical uncertainty and new trade tariffs continue to drive investors toward gold. (4)

Crypto Markets Overview

1. Main Assets

BTC Price

BTC Price

ETH Price

ETH Price

ETH/BTC Ratio

ETH/BTC Ratio

BTC fell 2.7% last week, while ETH declined 3.4%. After four consecutive weeks of net inflows, BTC spot ETFs finally saw a reversal, posting net outflows of $296.2M. ETH spot ETFs also recorded net outflows, totaling $206.6M. (5)

The ETH/BTC ratio edged down 0.7% over the week, while overall market sentiment remained deeply depressed, with the Fear & Greed Index still in Extreme Fear territory at 8. (6)

2. Total Market Cap

Crypto Total Marketcap

Crypto Total Marketcap

Crypto Total Marketcap Excluding BTC and ETH

Crypto Total Marketcap Excluding BTC and ETH

Crypto Total Marketcap Excluding Top 10 Dominance

Crypto Total Marketcap Excluding Top 10 Dominance

Total crypto market cap declined 2.5% last week. Excluding BTC and ETH, market cap fell 1.5%, indicating that weakness was broader than just the two majors. The altcoin market also edged lower, with total altcoin market cap down 0.7% over the same period.

Source: Coinmarketcap and Gate Ventures, as of 30th Mar 2026

Source: Coinmarketcap and Gate Ventures, as of 30th Mar 2026

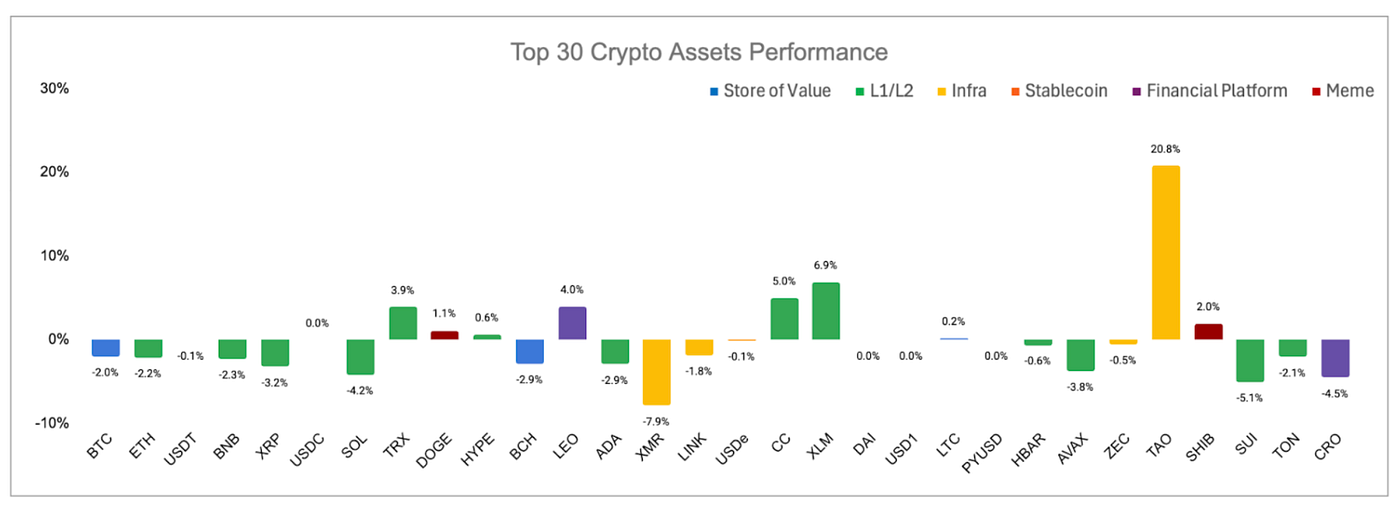

Among the top 30 assets, prices declined ~0.01% on average, TAO, XLM, CC have posted relatively significant gains.

TAO surged 20.8%, mainly driven by a sharp rally in subnet SN3. The key catalyst was SN3’s announcement that it had successfully trained Covenant-72B, a 72B-parameter LLM, through a distributed network of 70+ independent nodes without relying on centralized data centers. Sentiment was further boosted by Nvidia CEO Jensen Huang recently comparing Bittensor to a “modern-day Folding@home.” (7)

The Key Crypto Highlights

1. Walmart-backed OnePay expands token listings as crypto superapp strategy takes shape

OnePay, the fintech platform majority-owned by Walmart, has expanded its crypto offerings beyond Bitcoin and Ethereum by adding more than a dozen new tokens, including Solana, Cardano, Bitcoin Cash, PAX Gold, SUI, Polygon and Arbitrum. OnePay is a consumer financial app that offers services such as savings accounts, debit and credit products, payments, loans and a digital wallet that can be used across Walmart’s ecosystem, positioning itself as a US-style “superapp” for everyday financial activity. The company said it is prioritizing assets with strong customer demand, liquidity, regulatory clarity and long-term utility, rather than simply chasing new listings. (8)

2. BNP Paribas adds crypto ETNs for French retail clients as European bank distribution broadens

BNP Paribas is expanding its digital asset offering by adding six Bitcoin- and Ether-linked exchange-traded notes for retail clients in France, giving investors regulated exposure to BTC and ETH through standard securities accounts. The products will be available to individual investors, entrepreneurs, private banking clients and Hello bank! users, with potential expansion to wealth management clients outside France. The move is notable because it reflects continued growth in crypto ETN adoption across Europe, while also reinforcing BNP Paribas’ broader digital asset strategy spanning tokenized bonds, tokenized funds and institutional blockchain infrastructure such as Canton Network. (9)

3. Tether moves toward first full USDT audit as transparency push and US ambitions deepen

Tether has reportedly hired KPMG to conduct its first full independent audit of USDT’s financial statements, with PwC assisting on internal systems preparation, marking a major step beyond the reserve attestations it has relied on in recent years. The reported engagement comes as Tether looks to strengthen credibility ahead of a potential US expansion under the new federal stablecoin framework and as it reportedly explores a large equity raise. (10)

Key Ventures Deals

1. NYSE-parent ICE invests $600M in Polymarket as exchange operators move deeper into prediction markets

Intercontinental Exchange, the parent company of the New York Stock Exchange, has invested $600 million in Polymarket as part of its previously announced plan to commit up to $2 billion to the company. The investment is part of Polymarket’s latest funding round, with valuation details expected to be disclosed once the raise is completed. The move is notable because it signals that major exchange operators are increasingly viewing prediction markets as a meaningful new growth vertical, with the potential to expand retail participation, boost trading volumes and diversify revenue beyond traditional futures and options markets. (11)

2. Tazapay raises $36M Series B as regulated stablecoin-linked payment infrastructure gains traction

Singapore-based cross-border payments firm Tazapay has raised a $36 million Series B extension led by Circle Ventures, with participation from CMT Digital and Coinbase Ventures alongside existing investors including Ripple, Peak XV and January Capital. The company said the new capital will be used to secure additional regulatory approvals and expand product development for automated payment flows, as it continues building infrastructure for cross-border business payments. It highlights growing investor conviction that regulated intermediaries such as Tazapay can become key connective tissue between traditional payment systems and stablecoin rails, particularly as cross-border payments shift toward more compliant, enterprise-focused adoption. (12)

3. Kairos raises $2.4M to build onchain interest rate swaps as DeFi fixed-income infrastructure matures

Kairos Labs has raised a $2.4 million seed round led by 6th Man Ventures to launch the interest rate swap protocol designed for the EVM, with mainnet launch on Ethereum and Base expected in the coming weeks. The protocol aims to let users create onchain markets for swapping fixed and floating rate exposure, addressing a major missing piece in DeFi credit infrastructure after a beta that already generated more than $300 million in notional swap volume. The move is notable because interest rate swaps are the core hedging layer that makes fixed-rate lending and fixed-income products possible in traditional finance, and bringing that functionality onchain could materially expand DeFi beyond variable-rate leverage into more institutional and duration-sensitive credit use cases. (13)

Ventures Market Metrics

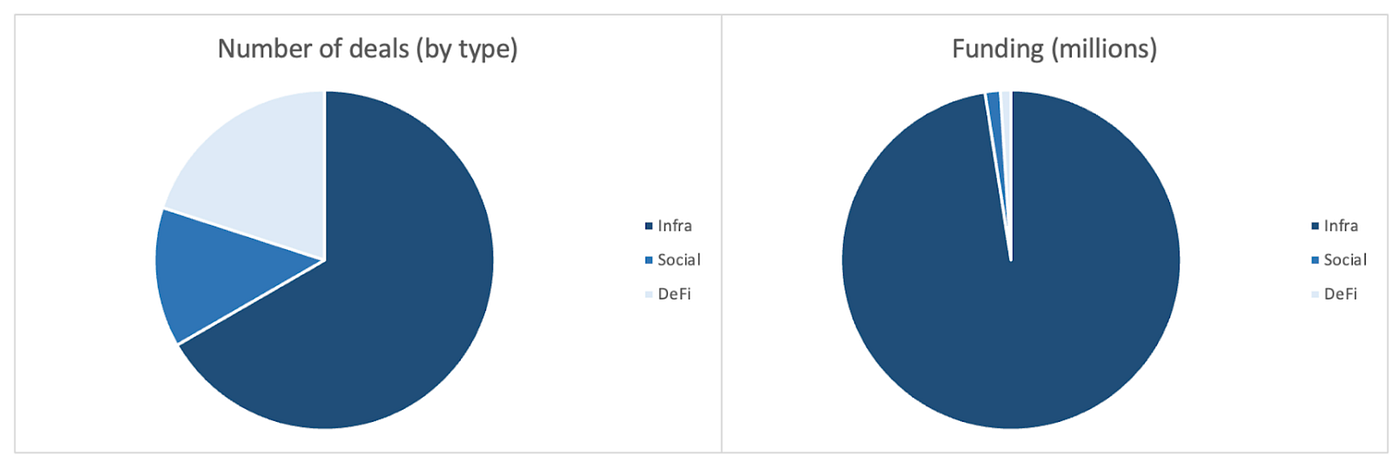

The number of deals closed in the previous week was 15, with Infra having 10 deals, representing 67% of the total number of deals. Meanwhile, Social had 2 deals, and DeFi had 3 deals.

Weekly Venture Deal Summary, Source: Cryptorank and Gate Ventures, as of 30th Mar 2026

Weekly Venture Deal Summary, Source: Cryptorank and Gate Ventures, as of 30th Mar 2026

The total amount of disclosed funding raised in the previous week was $731.7M, 3 deals in the previous week didn’t announce the raised amount. The top funding came from the Infra sector with $713.7M. Most funded deals: Polymarket ($600M).

Weekly Venture Deal Summary, Source: Cryptorank and Gate Ventures, as of 30th Mar 2026

Weekly Venture Deal Summary, Source: Cryptorank and Gate Ventures, as of 30th Mar 2026

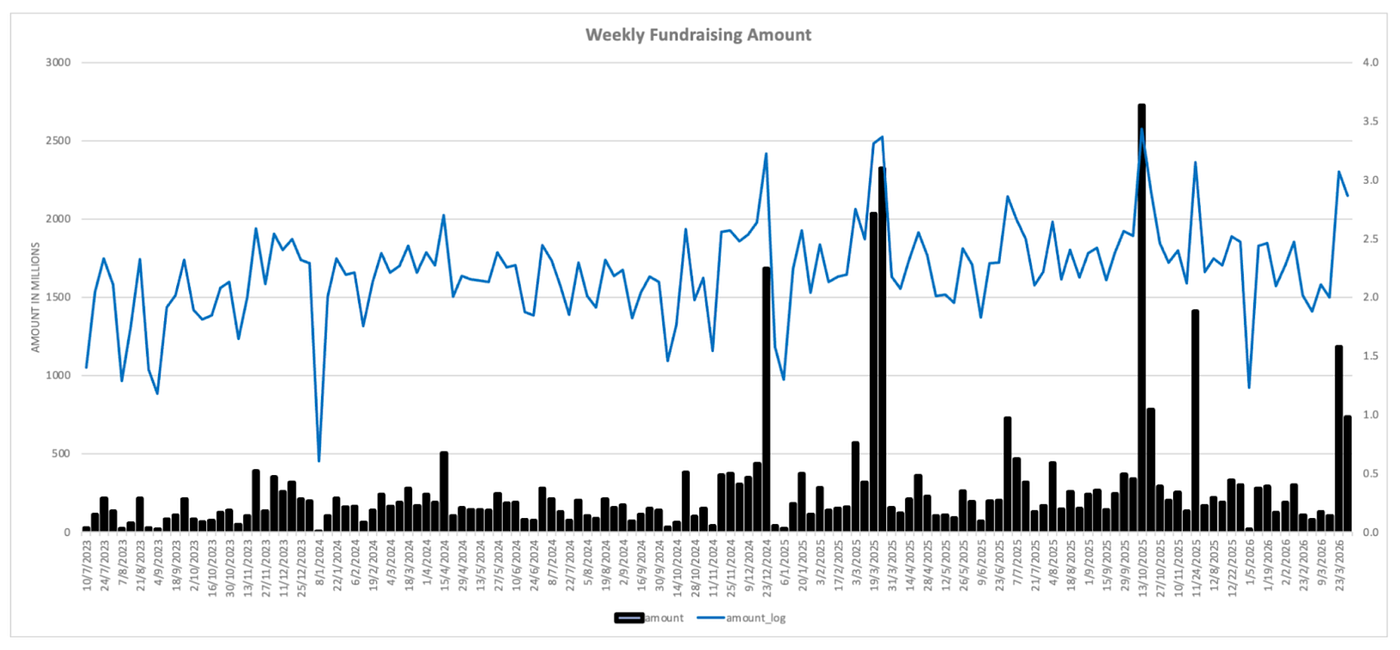

Total weekly fundraising declined to $731.7M for the fifth week of Mar-2026, a decrease of 38% compared to the week prior.

About Gate Ventures

Gate Ventures, the venture capital arm of Gate.com, is focused on investments in decentralized infrastructure, middleware, and applications that will reshape the world in the Web 3.0 age. Working with industry leaders across the globe, Gate Ventures helps promising teams and startups that possess the ideas and capabilities needed to redefine social and financial interactions.

Website | Twitter | Medium | LinkedIn

The content herein does not constitute any offer, solicitation, or recommendation*.* You should always seek independent professional advice before making any investment decisions. Please note that Gate Ventures may restrict or prohibit the use of all or a portion of the services from restricted locations. For more information, please read its applicable user agreement.

Reference:

- Trading Economic Ahead Economic Preview, https://tradingeconomics.com/calendar?article=29344&g=top&importance=2&startdate=2026-03-27

- DXY Index, TradingView, https://www.tradingview.com/chart/z1UD772v/?symbol=TVC%3ADXY

- US 10 Year Bond Yield, TradingView, https://www.tradingview.com/chart/B9cgEklh/?symbol=TVC%3AUS10Y

- Gold Price, TradingView, https://www.tradingview.com/chart/z1UD772v/?symbol=TVC%3AGOLD

- BTC & ETH ETF Inflow, https://sosovalue.com/tc/assets/etf/us-btc-spot

- BTC Greed and Fear Index, https://alternative.me/crypto/fear-and-greed-index/

- Announcement on Covenant-72B, https://x.com/opentensor/status/2032567840189096404

- Walmart-backed OnePay expands token listings as crypto superapp strategy takes shape, https://cointelegraph.com/news/walmart-backed-onepay-adds-a-dozen-new-tokens-in-push-to-serve-new-to-crypto-customers

- BNP Paribas adds crypto ETNs for French retail clients as European bank distribution broadens, https://cointelegraph.com/news/bnp-paribas-bitcoin-ether-etns-france-retail

- Tether moves toward first full USDT audit as transparency push and US ambitions deepen, https://cointelegraph.com/news/tether-long-awaited-audit-finally-lands-kpmg

- NYSE-parent ICE invests $600M in Polymarket as exchange operators move deeper into prediction markets, https://www.reuters.com/business/nyse-parent-intercontinental-exchange-invests-600-million-polymarket-2026-03-27/

- Tazapay raises $36M Series B as regulated stablecoin-linked payment infrastructure gains traction, https://www.techinasia.com/news/tazapay-nets-36m-series-led-circle-ventures

- Kairos raises $2.4M to build onchain interest rate swaps as DeFi fixed-income infrastructure matures, https://chainwire.org/2026/03/25/kairos-raises-2-4m-to-bring-the-500t-swap-market-onchain/