Traditional payment systems rely heavily on banking networks and clearing institutions to process cross-border transactions, such as SWIFT and correspondent banking models. While these systems are mature and stable, they face structural limitations including long settlement cycles, high fees, operational complexity, and reliance on intermediary trust.

Plasma (XPL) is positioned as a stablecoin-based payment infrastructure. Rather than replacing the entire financial system, its objective is to redesign the payment and settlement layer. By enabling on-chain settlement, using stablecoins as the core settlement asset, and optimizing transaction costs through protocol-level mechanisms, Plasma introduces a payment model that reduces reliance on intermediaries and connects traditional finance with the crypto economy.

Payment Mechanisms: Account-Based Clearing vs Direct Asset Transfer

Traditional payment networks operate on an “account-based + intermediary clearing” model. Transfers between users are essentially updates to bank ledgers, requiring confirmation across multiple intermediaries.

In contrast, Plasma adopts an on-chain “direct asset transfer” model. Users hold stablecoins directly, and transferring assets represents a change in ownership recorded on-chain. Settlement and clearing occur simultaneously within a single transaction flow, eliminating intermediate steps and reducing operational complexity.

Core Comparison: Plasma vs Traditional Payment Networks

Plasma (XPL) and traditional banking-based payment systems differ significantly across settlement, cost, and operational efficiency.

Compared to traditional systems that rely on multi-layer clearing and bank intermediaries, Plasma uses on-chain settlement and smart contract programmability to reduce settlement time from days to seconds or minutes. Its 24/7 operation and low entry barriers make it more flexible and efficient in a global financial context.

| Dimension |

Plasma (XPL) |

Traditional Payment Systems |

| Settlement Method |

Direct on-chain settlement (asset transfer) |

Multi-layer clearing (account-based ledger updates) |

| Settlement Speed |

Seconds to minutes |

1–5 business days |

| Transaction Cost |

Low (gas + network fees) |

High (transfer fees + intermediary fees + FX spreads) |

| Intermediary Dependence |

No intermediaries required |

Highly dependent on banking systems |

| Liquidity Management |

Unified on-chain liquidity |

Pre-funded accounts (Nostro/Vostro) |

| Programmability |

Supports smart contracts |

Limited or no programmability |

| Accessibility |

Accessible via a crypto wallet |

Requires a bank account |

| Operating Hours |

24/7 |

Limited by banking hours |

Settlement Speed

Traditional systems typically require one to five business days for cross-border settlement, depending on intermediary layers and time zones.

Plasma (XPL) enables near real-time settlement, with transactions confirmed within seconds or minutes.

Cost Structure

Traditional cross-border payments involve multiple fees, including transfer charges, intermediary bank fees, and foreign exchange spreads.

Plasma’s costs are primarily based on on-chain gas and infrastructure fees, resulting in significantly lower overall costs, especially for high-frequency transactions.

Liquidity Management

Traditional systems depend on pre-funded accounts such as Nostro and Vostro, which reduce capital efficiency.

Plasma uses stablecoins to unify liquidity on-chain, allowing funds to be allocated dynamically without pre-positioning capital across multiple accounts. This improves capital efficiency and enables real-time settlement.

Programmability

Traditional payment systems have limited flexibility and struggle to support automated logic.

Plasma enables programmable payments through smart contracts, allowing automated settlement, conditional payments, batch transfers, and multi-party workflows.

Accessibility

Traditional systems require bank accounts and are subject to regional and institutional constraints.

Plasma only requires a blockchain wallet, significantly lowering access barriers for global users.

Evolution of Cross-Border Payments: From Transfers to Value Networks

Cross-border payments are evolving from simple asset transfers to programmable value networks.

In traditional systems, payments primarily function as a transfer mechanism. In Plasma, payments can embed logic, such as automated trade settlement, real-time revenue sharing, and multi-party coordination. This transformation shifts payment infrastructure into a programmable financial layer.

Plasma as a Complement to Traditional Systems

Plasma is not designed to fully replace traditional payment networks. Instead, it complements and enhances the settlement layer.

In practice, on-chain systems handle efficient settlement, while off-chain systems continue to manage fiat on-ramps, compliance, and regulatory requirements. This hybrid model combines efficiency with stability, enabling gradual upgrades to global payment infrastructure without disrupting existing systems.

Advantages and Limitations

Although Plasma reflects a strong focus on maximizing payment efficiency through decentralized technology, traditional payment systems continue to dominate today's market due to decades of accumulated stability. The following outlines the respective advantages and limitations of both systems.

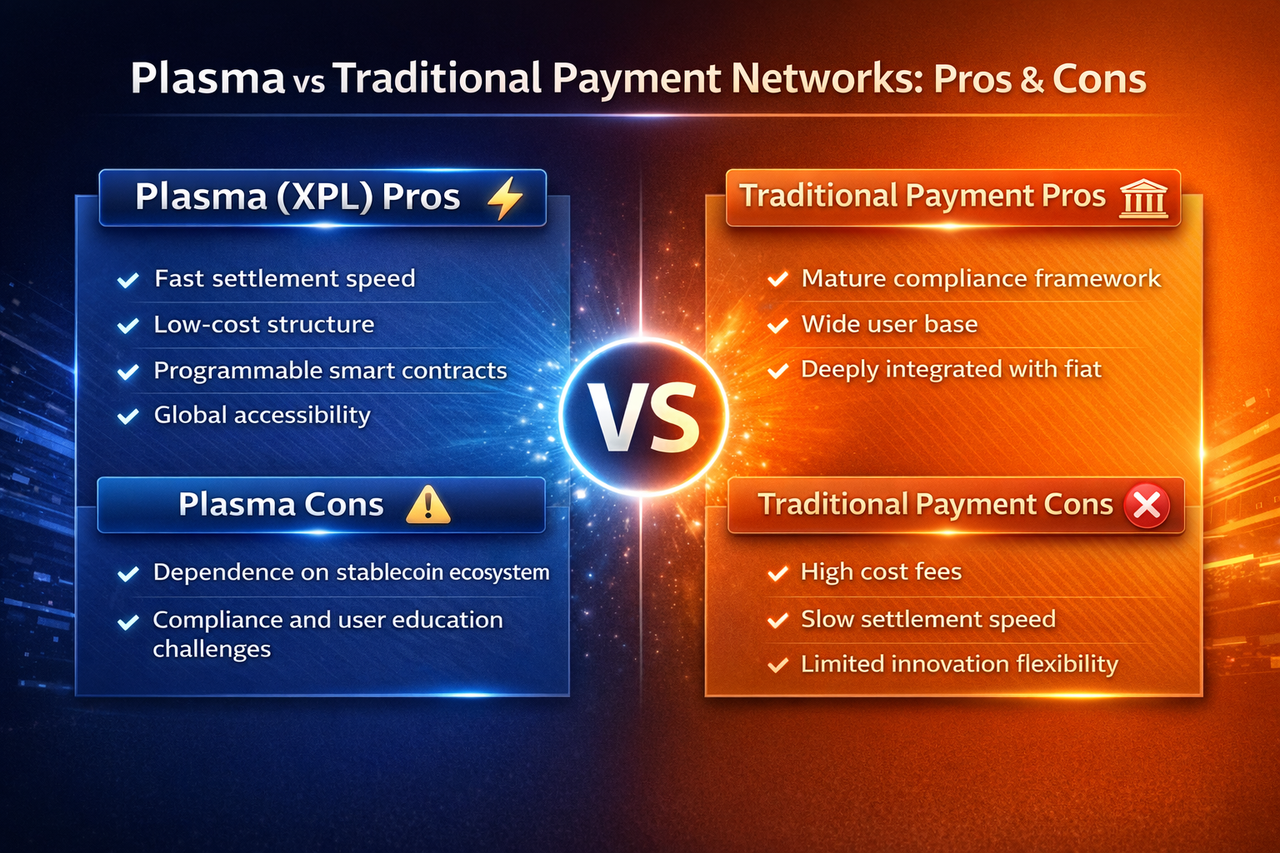

Plasma Advantages

Plasma offers significant improvements in settlement speed and cost efficiency. Its on-chain design enables near real-time transfers with lower fees, reduces reliance on intermediaries, and supports programmable financial logic. Its global accessibility further enhances its potential adoption.

However, Plasma also faces limitations. Its growth depends on stablecoin adoption, and regulatory frameworks remain uncertain. Additionally, user onboarding and usability challenges may slow adoption among non-crypto users.

Traditional System Advantages

Traditional payment systems benefit from mature regulatory frameworks, widespread adoption, and integration with fiat currencies. They remain highly reliable for large-scale financial and commercial operations.

However, their limitations include high costs, slow settlement, capital inefficiencies due to pre-funded accounts, and limited flexibility in adapting to new digital economic models.

Conclusion

The core difference between Plasma (XPL) and traditional payment systems lies in whether settlement depends on intermediaries or occurs directly on-chain. Plasma emphasizes efficiency, low cost, and global liquidity, while traditional systems prioritize compliance, security, and stability.

In the future, global payment infrastructure is more likely to evolve through the integration of both models rather than complete replacement. Plasma optimizes how value moves, while traditional systems ensure how value moves within regulatory frameworks. Together, they form a complementary structure for the next generation of global payments.

FAQs

Will Plasma replace traditional banking systems?

In the short term, no. Plasma is more likely to complement existing systems, particularly at the payment and settlement layer.

Is Plasma suitable for all payment scenarios?

It is currently best suited for cross-border payments, high-frequency transactions, and stablecoin-based transfers. Fiat-only payments still rely on traditional systems.

What are the main risks of Plasma?

Key risks include regulatory uncertainty, stablecoin-related risks, and security challenges within on-chain infrastructure.

Why is Plasma more efficient for cross-border payments?

Because it enables direct on-chain settlement, reducing intermediaries and allowing real-time capital movement.