Chris Dixon из a16z: Stablecoins — Делаем деньги текучими, как информация

В начале 2024 года Крис Диксон из a16z опубликовал “Read Write Own”, манифест, направляющий нас в третью эру Интернета — Web3, Интернета ценности. В предыдущих поколениях веба информация могла передвигаться по всему миру: мгновенно, бесплатно и без границ.

С Web3 акцент смещается на 'собственность'. Теперь у нас есть возможность демократизировать и монетизировать информацию, а также обеспечить свободное и легкое движение денег и ценности по всему миру через технологию блокчейн.

Хотя видение вдохновляет, реальность остается сложной. Даже в 2025 году мы все еще сталкиваемся с фундаментальным вопросом:

Если Интернет сделал поток информации свободным и глобальным, почему перемещение денег все еще так затруднительно и дорого?

Крис Диксон предлагает, что стейблкоины, построенные на блокчейн-сетях, предлагают решение.

Стейблкоины впервые дают нам реальную возможность трансформировать деньги так радикально, как это сделало электронное письмо с коммуникацией, делая ее открытой, мгновенной и безграничной. Это момент WhatsApp для передачи стоимости: глобальная сеть, построенная на блокчейне и стейблкоинах, которая может принести пользу всем.

Для более глубокого изучения этого вопроса мы собрали недавнюю статью Криса Диксона «Стейблкоины: Платежи без посредников», а также его более раннее произведение «Манифест Read Write Own», чтобы лучше понять логику основополагающую свободное движение информации и ценности по мере того, как мы входим в самое сердце Интернета ценности Web3.

1. Интернет ценности Web3

Интернет, вероятно, является одним из самых важных изобретений XX века, имеющим влияние, сопоставимое с изобретением печатного пресса, парового двигателя и электричества.

В отличие от многих ранних изобретений, Интернет не был немедленно коммерциализирован. Его ранние создатели не разрабатывали его как централизованную систему, а как открытую платформу, доступную каждому - художникам, пользователям, разработчикам, компаниям и другим.

По низкой цене и без необходимости получения разрешения кто угодно, где угодно, мог создавать и делиться кодом, искусством, письмом, музыкой, играми, веб-сайтами, стартапами — все, что угодно воображению.

И то, что ты создал, было твоим.

Пока вы следовали закону, никто не мог изменить ваши правила, взять большую долю или захватить вашу работу. Интернет был создан для того, чтобы быть разрешительным и демократически управляемым, как и его ранние сети - электронная почта и веб - где у никого не было особых привилегий. Любой мог инновировать на основе этих сетей и контролировать свою собственную творческую и экономическую судьбу.

Эта свобода и чувство собственности вызвали золотой век творчества и инноваций, питая рост Интернета и порождая бесчисленные приложения, которые изменили наш образ жизни, работу и развлечения.

Я вижу историю интернета как три отдельные фазы, каждая из которых определена основной сетевой архитектурой:

Первая фаза, Web1 (приблизительно 1990–2005 годы), была эпохой “Чтения”, когда ранние интернет-протоколы демократизировали доступ к информации. Любой мог ввести несколько слов в браузер и мгновенно прочитать о практически любой теме.

Вторая фаза, Web2 (около 2006–2020 гг.), была эрой "Write", где корпоративные платформы демократизировали публикации. Любой мог поделиться своими мыслями с миром через социальные сети и другие онлайн-сервисы.

Теперь новая архитектура поддерживает третью эру — Web3, Интернет ценности, ориентированный на «владение». Эта новая модель естественным образом сочетает в себе две предыдущие и демократизирует само владение. В грядущей эпохе «Читай Пиши Владей» каждый может быть заинтересованным лицом в сети, наслаждаясь правами и экономическими выгодами, ранее зарезервированными для внутренних сотрудников компании, таких как акционеры и сотрудники.

Люди могут читать и писать в Интернете, но теперь они могут действительно владеть.

(https://a16zcrypto.com/posts/article/read-write-own-intro/)

2. Потенциал дестабилизации стейблкоинов

Интернет обеспечил свободное и глобальное распространение информации. Почему же перемещение денег по-прежнему так сложно и дорого?

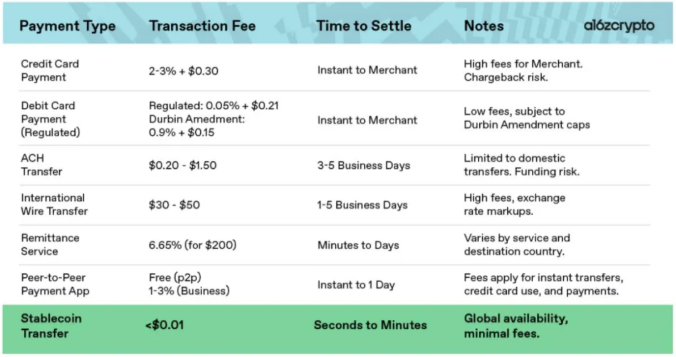

Существующие платежные системы не были созданы для Интернета; они были построены вокруг организаций, заполненных рентабельными посредниками - субъектами, которые когда-то управляли местными партнерствами, предотвращением мошенничества и операциями. Даже сейчас отправка денег за границу может обойтись вам дорого, до 10%. В сентябре 2024 года средняя комиссия за отправку $200 за границу составляла 6.62%. Эти сборы - это не просто трение, это фактически регрессивные налоги на некоторых из самых бедных людей в мире. Даже в наш век цифровых технологий платежные системы остаются медленными, непрозрачными и исключительными, оставляя миллиарды людей без должного обслуживания или полностью отрезанными от глобальной финансовой системы.

(Как стейблкоины поглотят платежи, и что произойдет дальше, a16z)

Для многих компаний неэффективность традиционных платежей является значительным бременем. Стейблкоины предлагают драматическое улучшение. Например, бизнес-платежи от Мексики во Вьетнам могут занимать 3–7 дней на расчеты, с комиссиями в пределах от $14 до $150 за $1,000, проходя через до пяти посредников, каждый из которых берет свою долю. Стейблкоины могут обойти устаревшие системы, такие как международная сеть SWIFT и ее сложные процессы клиринга и расчетов, делая эти транзакции почти бесплатными и практически мгновенными.

(Как стейблкоины поглотят платежи, и что произойдет дальше, a16z)

Это не только теоретический момент — это уже происходит. Например, SpaceX использует стейблкоины для управления своими корпоративными средствами, включая репатриацию денег из стран с волатильными валютами, такими как Аргентина и Нигерия. Другие компании, например, ScaleAI, используют стейблкоины для более быстрой и экономичной оплаты своего глобального персонала. На стороне потребителя Stripe является первым крупным сервисом, который широко предлагает криптовалютные платежи, взимая всего 1,5% комиссии при оформлении заказа — вдвое меньше, чем у традиционных поставщиков. Это может существенно увеличить прибыльные маржи для некоторых компаний: как отмечает Сэм Бронер из a16z crypto, для компаний с низкой рентабельностью, таких как продуктовые магазины, улучшение на 1,5% может удвоить чистую прибыль. И в конкурентной, основанной на блокчейне индустрии, расходы на транзакции, вероятно, еще больше снизятся.

(Как стейблкоины поглотят платежи, и что произойдет дальше, a16z)

В отличие от традиционных финансовых систем, стейблкоины по умолчанию являются глобальными. Они существуют на блокчейне, открытой и программируемой сети, где любой может создать — не нужно вести переговоры с десятками банков для международных транзакций. Все, что вам нужно, это доступ к сети.

Люди уже видят выгоду. В 2024 году стейблкоины переместили $15.6 триллиона стоимости — почти столько же, сколько обработал Visa. Хотя большинство из этого — потоки криптовалютных активов, а не розничные платежи, сам масштаб показывает, что мы на пороге революции финансовой инфраструктуры, которая не требует склейки устаревших систем 20 века.

Вместо этого мы можем построить что-то новое, действительно собственное для Интернета - или, как описывает это Stripe, «сверхпроводники при комнатной температуре для финансовых услуг». Здесь это не потери энергии, а потери стоимости.

3. Момент WhatsApp для денег

Стейблкоины представляют собой наш первый реальный шанс трансформировать деньги так же, как электронная почта произвела революцию в общении: сделав его открытым, мгновенным и безграничным.

Подумайте о том, как развивалась текстовая переписка. До появления приложений, таких как WhatsApp, отправка международного SMS-сообщения стоила 30 центов за сообщение, и даже в этом случае вам повезло, если оно пришло. Сейчас мы мгновенно отправляем сообщения через Интернет по всему миру и бесплатно. В сравнении сегодняшние платежи застряли там, где находилась текстовая переписка в 2008 году: раздробленные национальными границами, замедленные посредниками и ограниченные устаревшим дизайном.

Стейблкоины предлагают свежий старт. Вместо того, чтобы полагаться на устаревшие, дорогостоящие и громоздкие платежные системы, стейблкоины легко перетекают на глобальных блокчейнах. Эти блокчейны программуемы и комбинируемы, что делает их идеальными для создания решений, масштабирующихся за пределами границ.

Стейблкоины уже снизили стоимость международных денежных переводов. Например, отправка $200 из США в Колумбию традиционными методами стоит $12.13; используя стейблкоины, это всего один цент. Хотя конвертация стейблкоинов в местную валюту по-прежнему может стоить до 5%, конкуренция быстро снижает эти сборы.

Как и WhatsApp, который изменил дорогие международные звонки, блокчейн-платежи и стейблкоины преобразуют способы передвижения денег по всему миру.

4. Регулирование: от преграды к прорыву

Легко видеть регулирование как барьер, но умное законодательство может открыть совершенно новую эру.

Четкие правила для стейблкоинов и более широкого крипто-рынка наконец могут вывести эти технологии из песочницы и в основной поток. Децентрализованная финансовая (DeFi) существует в закрытом «крипто-крипто» цикле уже много лет — не потому что эти инструменты не имеют ценности, а из-за того, что регулирование затрудняет подключение к традиционной финансовой системе.

Это начинает меняться. Теперь законодатели разрабатывают правила для признания и регулирования стейблкоинов с целью сохранения конкурентоспособности США, защиты потребителей и содействия инновациям. Хорошо продуманное регулирование, такое как рамки, различающие между сетевыми токенами и ценными бумагами, может исключить плохих участников, предоставив ответственным игрокам необходимую ясность. Фактически, предстоящий законопроект, уточняющий регулирование стейблкоинов, может проложить путь для более широкого принятия и интеграции в глобальную финансовую систему.

5. Построение общественных благ, которые приносят пользу всем

Традиционная финансовая система построена на частных, закрытых сетях, но Интернет показал нам силу открытых протоколов, таких как TCP/IP и электронная почта, для содействия глобального сотрудничества и инноваций.

Блокчейны являются финансовым слоем Интернета, объединяющим гибкость общедоступных протоколов с экономической мощью частных предприятий. Они являются недоверчивыми, нейтральными, проверяемыми и программируемыми. Добавьте стабильные монеты, и вы получите то, чего у нас никогда действительно не было: открытую денежную инфраструктуру.

Думайте об этом как о системе общественных автомагистралей. Частные компании по-прежнему могут строить транспортные средства, вести бизнес и создавать достопримечательности вдоль маршрута, но сами дороги открыты для всех.

Сети блокчейн и стейблкоины - это не только снижение затрат. Они открывают новые способы оплаты:

Программируемые платежи: Представьте себе рынки, управляемые искусственным интеллектом, где агенты автоматически организуют платежи за вычислительные ресурсы и услуги. (Платежи Web3: Обзор программных платежей, программных денег и специализированных валют)

Микроплатежи за медиа, музыку и вклады в ИИ: Представьте, что вы устанавливаете бюджет и некоторые простые правила, а затем позволяете 'умному' кошельку обрабатывать распределение.

Прозрачные платежи с полным аудитом: Представьте, как эти системы используются для отслеживания государственных расходов.

Глобальный бизнес: Представьте себе мгновенное и практически бесплатное осуществление международных транзакций — на самом деле, это уже происходит.

Звёзды становятся на место для блокчейн-сетей и стейблкоинов: технологии, рыночный спрос и политический импульс все указывают на то, что эти приложения могут стать реальностью. В этом году может быть принят законопроект о стейблкоине, и регуляторы работают над рамками для соответствия риска соответствующему надзору.

6. Заключительные мысли

Так же, как ранние интернет-стартапы процветали, как только они узнали, что их не закроют телекоммуникационные компании или юристы по авторским правам, криптовалюта теперь готова перейти от финансового эксперимента к основной инфраструктуре, возглавляемой стейблкоинами.

Нам не нужно постоянно пытаться починить старые системы. Мы можем построить что-то лучшее.

Оговорка:

1.Эта статья перепечатана с [GateWeb3 Xiaolu]. All copyrights belong to the original author [Вилл Аванг]. Если есть возражения к этому перепечатыванию, пожалуйста, свяжитесь с Gate Learnкоманда, и они быстро справятся с этим.

2. Отказ от ответственности: Взгляды и мнения, высказанные в данной статье, являются исключительно точкой зрения автора и не являются инвестиционным советом.

3. Переводы статьи на другие языки выполняются командой Gate Learn. Если не указаноGate.com, копирование, распространение или плагиат переведенных статей запрещены.

Пригласить больше голосов

Содержание

Похожие статьи

Что такое стейблкоин?

Что такое USDe? Раскрываются множественные методы заработка USDe

Что такое USDT0

Новый стейблкоин USDT0 от Tether: В чем его отличие от USDT?

Глубокое объяснение Yala: построение модульного агрегатора доходности DeFi с устойчивой монетой $YU в качестве средства обмена